1. The Promissory Note - a pattern of fraud.

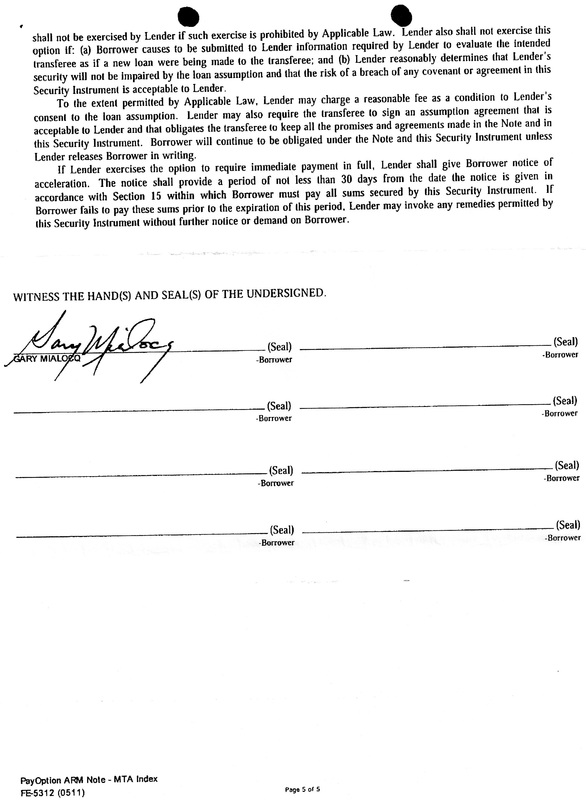

The "Original" Promissory Note (which I always took to mean there was only ONE ) is what creditors traditionally must produce in court to prove they are entitled to receive payments and that they are the true owner of the debt. Oh was I wrong! I sent what is called a RESPA Letter to ONE WEST BANK which requires them to provide certain documents including a fresh copy of the original promissory note. This is what they sent to me. Notice on the first signature line on the left, that there are no endorsements, only my signature. Also take note for further comparison, that the tail of the "y" in my first name goes directly through the "C".

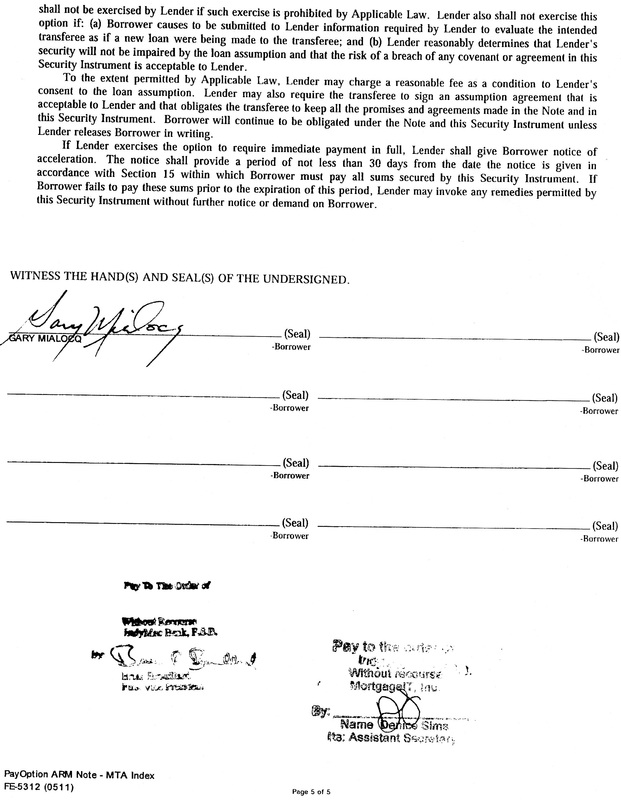

During the course of my interaction with ONE WEST BANK they filed three (3) more copies of the EXACT SAME document (easily determined by examining my signature). Each "original' bore a different endorsement or set of endorsements. All were filed in Federal court. I have posted copies of the four "originals" below. The first from the left is the blank endorsement I received from IndyMac when I requested a copy of the original. The second is endorsed by a Denice Sims of MortgageIT.

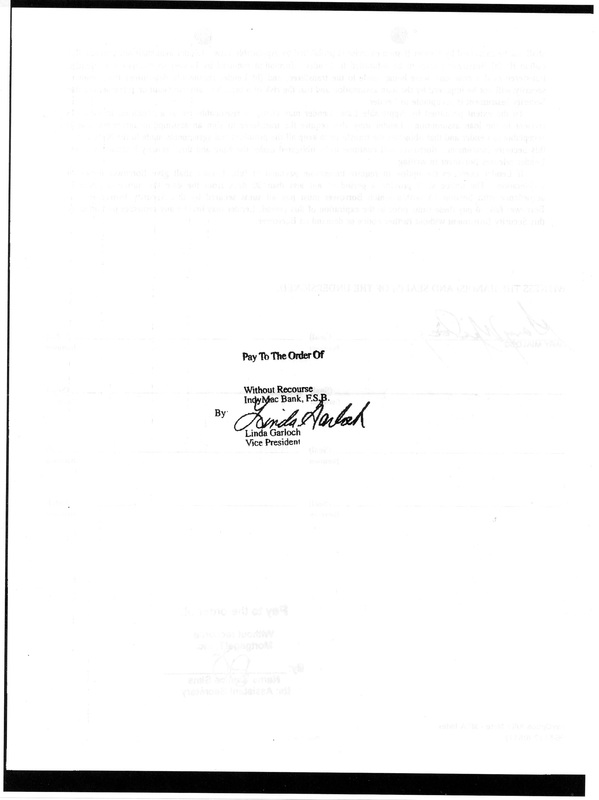

The next "original" had Ms. Sims' signature on the front, along with an endorsement by Linda Narlock, a VP at Indymac Bank on the back. Ms. Narlock's signature is evident on the fourth document from the left.

The most damning evidence of intentional fraud is the third original. It again shows Ms. Sims's signature, but this time, apparently unaware of the endorsement on the back, another officer at Indymac Bank with the initials "B.B." endorsed the front. That's a total of four (4) different "originals" of my note that were filed in Court. I called attention to this fact to the court on several times and they flat-out ignored it. Judge Baum would sit there and listen but never comment and just move on to the next topic.

Think about that. A Federal Bankruptcy Court judge ignored the fact that ONE WEST BANK had doctored an original document multiple times in an attempt to prove that they were the legal owners. Not only did they alter the documents, but they actually filed them in court. In addition, two attorneys swore under oath that they had seen the original blue-ink document which they clearly had not.

EVIDENCE

According to a Deposition submitted by a ONE WEST BANK attorney, Ryan Shawn Patterson, ONE WEST BANK provided the “original” Promissory Note to their attorneys on Dec. 15, 2010, which they they then filed. Mr. Patterson claims that there were TWO endorsements on the face of the Note, and that he returned the originals to ONE WEST BANK and served his copy upon the Court. He is referring to the third document from the left pictured below. I believe he is telling the truth. However, the “original” furnished to him by ONE WEST BANK in December, 2010, is VERY DIFFERENT from that submitted by ONE WEST BANK to their previous attorney and then to this Court on 3/2/2010.

ONE WEST BANK served the following exhibit to the court along with its Motion to Avoid the Lien on 3/2/2010. Curiously, despite the description of two endorsements on the front by Mr. Patterson, there is only ONE allonge or endorsement on this one a year earlier. The endorsement on the document filed by Defendants on 3/2/2010 is pictured in #2.

This is the endorsement filed by ONE WEST BANK this week (Jan 2011): The signatures of Gary Mialocq and the stamp of Denice Sims are identical on both documents. The additional “endorsement” had to have been placed on this “original” document in the past year, which means it has been altered. Why did they do this? It was no accident. Because the “original” document supplied to the Court on 3/2/2010 had an allonge stamped on the back that apparently nobody noticed, and the current “original” lacked an IndyMac endorsement in front, someone at ONE WEST BANK in the last year decided to add an endorsement. Here is the endorsement from 3/2/2010 pictured in #3. Ooops!

In fact, this document has been altered more than once. On two previous occasions, Mialocq has been furnished copies of the “original”, both blank with no endorsements, yet Mialocq's signature is IDENTICAL to his on the subsequent documents. More proof that a single document has been altered.

According to Arizona Law, 47-3407 (2)(b), “an alteration fraudulently made discharges a party whose obligation is affected by the alteration.”

Why was ONE WEST BANK so desperate to prove standing that it became necessary to attempt to

assign title to themselves through MERS with a bogus signature by their own employee one year AFTER I had filed bankruptcy, and more than 3 years after the original documents were signed? Simple. It doesn't take a rocket scientist to figure out that they don't own the Note, and are not holders or parties in interest, and never were.

By trying to transfer the Deed of Trust and the Note from MERS to ONE WEST BANK, ONE WEST BANK admits that on 3/2/2010, it WAS NOT a holder of the Note, nor a Real Party in Interest at that time, or a transfer would not have been necessary. Furthermore, MERS has publicly stated that they do not hold Notes.

The United States Bankruptcy Court for the Eastern District of California, in the matter of Walker #10-21656-E-11, ruled as follows and it is spot on-in this case:

“Since no evidence of MERS' ownership of the underlying Note has been offered, and other courts

have concluded that MERS does not own the underlying Notes, this court is convinced that MERS

had no interest it could transfer... Since MERS did not own the underlying Note, it could not transfer the beneficial interest of the Deed of Trust to another. Any attempt to transfer the beneficial interest of a trust deed without ownership of the Note is void under state laws.”

Furthermore, MERS' own website has stated that they are not, and were not, the true beneficiary thereby nullifying any nomination to ONE WEST BANK. Therefore, the 1st Deed of Trust is invalid for the reasons stated above, and ONE WEST BANK has no standing whatsoever.

During the course of my interaction with ONE WEST BANK they filed three (3) more copies of the EXACT SAME document (easily determined by examining my signature). Each "original' bore a different endorsement or set of endorsements. All were filed in Federal court. I have posted copies of the four "originals" below. The first from the left is the blank endorsement I received from IndyMac when I requested a copy of the original. The second is endorsed by a Denice Sims of MortgageIT.

The next "original" had Ms. Sims' signature on the front, along with an endorsement by Linda Narlock, a VP at Indymac Bank on the back. Ms. Narlock's signature is evident on the fourth document from the left.

The most damning evidence of intentional fraud is the third original. It again shows Ms. Sims's signature, but this time, apparently unaware of the endorsement on the back, another officer at Indymac Bank with the initials "B.B." endorsed the front. That's a total of four (4) different "originals" of my note that were filed in Court. I called attention to this fact to the court on several times and they flat-out ignored it. Judge Baum would sit there and listen but never comment and just move on to the next topic.

Think about that. A Federal Bankruptcy Court judge ignored the fact that ONE WEST BANK had doctored an original document multiple times in an attempt to prove that they were the legal owners. Not only did they alter the documents, but they actually filed them in court. In addition, two attorneys swore under oath that they had seen the original blue-ink document which they clearly had not.

EVIDENCE

According to a Deposition submitted by a ONE WEST BANK attorney, Ryan Shawn Patterson, ONE WEST BANK provided the “original” Promissory Note to their attorneys on Dec. 15, 2010, which they they then filed. Mr. Patterson claims that there were TWO endorsements on the face of the Note, and that he returned the originals to ONE WEST BANK and served his copy upon the Court. He is referring to the third document from the left pictured below. I believe he is telling the truth. However, the “original” furnished to him by ONE WEST BANK in December, 2010, is VERY DIFFERENT from that submitted by ONE WEST BANK to their previous attorney and then to this Court on 3/2/2010.

ONE WEST BANK served the following exhibit to the court along with its Motion to Avoid the Lien on 3/2/2010. Curiously, despite the description of two endorsements on the front by Mr. Patterson, there is only ONE allonge or endorsement on this one a year earlier. The endorsement on the document filed by Defendants on 3/2/2010 is pictured in #2.

This is the endorsement filed by ONE WEST BANK this week (Jan 2011): The signatures of Gary Mialocq and the stamp of Denice Sims are identical on both documents. The additional “endorsement” had to have been placed on this “original” document in the past year, which means it has been altered. Why did they do this? It was no accident. Because the “original” document supplied to the Court on 3/2/2010 had an allonge stamped on the back that apparently nobody noticed, and the current “original” lacked an IndyMac endorsement in front, someone at ONE WEST BANK in the last year decided to add an endorsement. Here is the endorsement from 3/2/2010 pictured in #3. Ooops!

In fact, this document has been altered more than once. On two previous occasions, Mialocq has been furnished copies of the “original”, both blank with no endorsements, yet Mialocq's signature is IDENTICAL to his on the subsequent documents. More proof that a single document has been altered.

According to Arizona Law, 47-3407 (2)(b), “an alteration fraudulently made discharges a party whose obligation is affected by the alteration.”

Why was ONE WEST BANK so desperate to prove standing that it became necessary to attempt to

assign title to themselves through MERS with a bogus signature by their own employee one year AFTER I had filed bankruptcy, and more than 3 years after the original documents were signed? Simple. It doesn't take a rocket scientist to figure out that they don't own the Note, and are not holders or parties in interest, and never were.

By trying to transfer the Deed of Trust and the Note from MERS to ONE WEST BANK, ONE WEST BANK admits that on 3/2/2010, it WAS NOT a holder of the Note, nor a Real Party in Interest at that time, or a transfer would not have been necessary. Furthermore, MERS has publicly stated that they do not hold Notes.

The United States Bankruptcy Court for the Eastern District of California, in the matter of Walker #10-21656-E-11, ruled as follows and it is spot on-in this case:

“Since no evidence of MERS' ownership of the underlying Note has been offered, and other courts

have concluded that MERS does not own the underlying Notes, this court is convinced that MERS

had no interest it could transfer... Since MERS did not own the underlying Note, it could not transfer the beneficial interest of the Deed of Trust to another. Any attempt to transfer the beneficial interest of a trust deed without ownership of the Note is void under state laws.”

Furthermore, MERS' own website has stated that they are not, and were not, the true beneficiary thereby nullifying any nomination to ONE WEST BANK. Therefore, the 1st Deed of Trust is invalid for the reasons stated above, and ONE WEST BANK has no standing whatsoever.

|

|

|

|

False Claims - Attorney Perjury

On page 3, lines 15-16, of the MOTION TO LIFT THE AUTOMATIC STAY, and on page 3, lines 21-22 of her RESPONSE TO DEBTOR'S MOTION TO AVOID LIEN, Defendant's attorney makes the following statement: “ONE WEST BANK FSB is now the holder of the Note that is Secured by the Deed of Trust and is the real party in interest.” Attorney Arturo Thompson testified that he has personal knowledge that ONE WEST BANK is the Real Party in Interest. The documents prove otherwise as he, too, appears to have been conned.

IndyMac Bank also did not comply with the Fair Debt Collection Practices Act, 15 O.S.C. #1692(g), when it sent a “welcome” letter and did not provide a notice that included the amount of the debt, the creditor to whom the debt was owed, procedures for disputing the debt, and a statement verifying its validity. ONE WEST BANK has admitted this by entering into a Class Action settlement with many thousands of victimized borrowers. I would have declined the $24 settlement offer had I received notice of its existence in a timely fashion.

FACTS AND RULES GOVERNING CUSTODIAL CARE OF NOTES

Title 34 Section 674.19 (B)(4) & (B)(4)(i) of the US Code of Federal Regulations (CFR) states:

re. *Manner of Retention of Promissory Notes and Repayment Schedules: An institution shall keep the original promissory note and repayment schedule until the loan is satisfied. If required to release original documents in order to enforce the loan, the institution MUST retain certified true copies of those documents [i.e…if they do in fact possess, and are forced to release, the true original]. This does not mean that they can offer and act upon the "true copy" that they must keep by law, in lieu of presenting the original. *

*(i) An institution shall keep the original paper promissory note or original paper Master Promissory Note (MPN) and repayment schedules in a locked, fireproof container (in order to use them if ever needed, because 'copies' won't legally do the job). It is they, the holder of the note, who must submit the original and keep a copy -- not the other way around.*

I would say that's pretty specific and clear. They have a fiduciary duty to protect the original note according to the law. By submitting altered Promissory Notes and bogus Assignments of Deed of Trust, a logical person could only conclude that ONE WEST BANK is neither the holder of the Note nor the Real Party in Interest, which status it MUST hold in order to legally collect payments or proceed with foreclosure.

ASSIGNMENTS OF DEEDS OF TRUST

IndyMac Bank also did not comply with the Fair Debt Collection Practices Act, 15 O.S.C. #1692(g), when it sent a “welcome” letter and did not provide a notice that included the amount of the debt, the creditor to whom the debt was owed, procedures for disputing the debt, and a statement verifying its validity. ONE WEST BANK has admitted this by entering into a Class Action settlement with many thousands of victimized borrowers. I would have declined the $24 settlement offer had I received notice of its existence in a timely fashion.

FACTS AND RULES GOVERNING CUSTODIAL CARE OF NOTES

Title 34 Section 674.19 (B)(4) & (B)(4)(i) of the US Code of Federal Regulations (CFR) states:

re. *Manner of Retention of Promissory Notes and Repayment Schedules: An institution shall keep the original promissory note and repayment schedule until the loan is satisfied. If required to release original documents in order to enforce the loan, the institution MUST retain certified true copies of those documents [i.e…if they do in fact possess, and are forced to release, the true original]. This does not mean that they can offer and act upon the "true copy" that they must keep by law, in lieu of presenting the original. *

*(i) An institution shall keep the original paper promissory note or original paper Master Promissory Note (MPN) and repayment schedules in a locked, fireproof container (in order to use them if ever needed, because 'copies' won't legally do the job). It is they, the holder of the note, who must submit the original and keep a copy -- not the other way around.*

I would say that's pretty specific and clear. They have a fiduciary duty to protect the original note according to the law. By submitting altered Promissory Notes and bogus Assignments of Deed of Trust, a logical person could only conclude that ONE WEST BANK is neither the holder of the Note nor the Real Party in Interest, which status it MUST hold in order to legally collect payments or proceed with foreclosure.

ASSIGNMENTS OF DEEDS OF TRUST